Published by: Tray Traynor, CIC

Executive Summary

The report was prepared by the Pritchard & Jerden Senior Living & M&A Insurance practice group, which is led by Tray Traynor. Tray can be reached at 404-949-1072 or ttraynor@pjins.com.

RWI is expected to become a commonly utilized tool in senior housing transactions as education and awareness grows among buyers and sellers. Enclosed is information regarding the following topics:

1. What is Reps & Warranty Insurance (RWI)

2. RWI benefits to buyer and seller

3. Why to use RWI on senior housing transactions

4. Why not to use RWI on senior housing transactions

5. What reps does RWI cover on senior housing transactions

6. The RWI underwriting process

7. RWI Policy Structure & Pricing

8. Diligence Required

9. Why Pritchard & Jerden

10 .Pro-forma/Cost and Structure Example: $100,000,000 Deal

11. Pro-forma/Cost and Structure Example: $30,000,000 Deal

1. What is Reps & Warranty Insurance (RWI)?

- RWI is an insurance policy utilized by M&A professionals as a tool to enhance the M&A process, and to provide benefits to both buyer and seller. See benefits listed on the following page.

- The use of RWI in general M&A has increased by ~900% since 2013. PE groups use RWI on over 90+% of their acquisitions. RWI is used on ~50% of acquisitions by strategics, and that number continues to grow every year.

- The most significant increase in RWI utilization happened in 2014 when M&A professionals became comfortable that carriers would pay claims and started to see claims getting paid.

- Healthcare in general has been slower to adopt RWI primarily because initially, RWI didn’t cover Medicare/Medicaid reps. However, that has now changed. Coverage for Medicare/Medicaid (and other reps initially excluded) is now available. Please see this article which explains why RWI for healthcare “is a must”.

- There are approximately 25 RWI carriers in the marketplace today, and ~30-50% of those carriers have an appetite for healthcare/senior housing deals.

- Limit capacity for any individual RWI policy is north of $1 billion.

2. RWI Benefits to Buyer & Seller

Buyer Benefits

- RWI policy limit replaces the seller holdback/escrow

- RWI enhances buyer’s bid as it eliminates the holdback, which maximizes upfront proceeds

- RWI reduces post-closing liabilities

- Sellers are increasingly requesting RWI on bids – buyers will have to match request even if not in a competitive process

- Longer survival period (3-6 years) vs. standard escrow (12-18 mos.)

- RWI is a tool that buyers use to stay competitive in the auction process

- Reduces the amount of negotiation required on reps in the agreement

- Empirically and experientially, buyers now feel it is easier to recover for breaches of seller reps using RWI than from a traditional escrow

- Protects relationship with rolling shareholders and management team

- Helps facilitate cross-border transaction if the seller is in a suspect jurisdiction

Seller Benefits

- Significantly reduces (99.5%), or completely eliminates seller escrow, which maximizes upfront proceeds

- Seller realizes the full value of sale immediately / can redistribute funds faster

- Reduces post-closing liabilities/seller no longer liable for breach of reps post-closing

- Reduces the amount of negotiation required on reps in the agreement

- Helps facilitate the transaction if the buyer is suspect of the seller on any one particular rep

- Mitigates disparate seller situations

3. Why use RWI for senior housing transactions?

- The primary reason to consider RWI is because in today’s market it can help distinguish your bids by eliminating the holdback, which increases upfront proceeds, and it also reduces post-closing liabilities.

- Sellers are increasingly requiring RWI on their bid packages, so buyers are having to match that request and implement RWI.

- We predict RWI for senior housing will have a similar trajectory to that of RWI in general M&A. Therefore, senior housing buyers currently have a window of opportunity they can use to their advantage before the rest of the senior housing acquisition market catches up.

- What was the general M&A trajectory? Circa 2013, certain Private Equity groups utilized RWI to their advantage on bids before the market caught up. By 2015, the market had shifted to the point whereby if a buyer did not automatically include RWI terms with their bid, they would not be considered.

- How does RWI help distinguish a bid? If a seller has two bids otherwise equal, but one bid includes RWI, sellers typically prefer not having a holdback and will take the bid with RWI included.

4. Why not use RWI for senior housing transactions?

- Holdback percentages for senior housing transactions tend to be slightly lower than that of general M&A, which reduces the seller benefits a little. This does not affect the buyer benefits.

- Why pay the RWI premium if sellers aren’t requiring it, and competitors aren’t including it (we predict this dynamic will be short-lived as sellers are increasingly requesting RWI.)

- Lack of awareness on the process and how claims get paid.

5. What reps does RWI cover for senior housing transactions?

- RWI can be used on SNF’s, AL, IL, and standalone MC transactions.

- The RWI market has more capacity for AL/IL/MC transactions than for SNF transactions.

- RWI can be used if the deal includes Propco only, or PropCo + Opco

Propco only the typical reps covered and areas diligenced are:

- Fundamental reps of title, ownership, authority

- Environmental

- Structural condition of assets

- Financial reps (where applicable)

- Tax reps (where applicable)

Propco + Opco the typical reps covered and areas diligences are:

- Reps pertaining to property (see above)

- Financial statements and tax

- General management of the facility

- Medicare/Medicaid

- Stark/AKS compliance

- Billing/coding

- HIPAA

- FLSA/Wage & Hour/Employee Benefits

- Commercial Insurance Program

- Cyber/Privacy liability

6. RWI Underwriting Process

The RWI underwriting process is divided into three phases:

- Pre-underwriting

- Phase II underwriting

- Phase III underwriting

1) Pre-underwriting

- When either a buyer or seller contacts P&J for initial pricing and coverage expectations on a particular deal.

2) Phase I underwriting

- P&J approaches the RWI marketplace and produces an Indication Comparison Analysis (ICA) to compare term sheets. Phase I takes 2-5 days.

3) Phase II underwriting

- Phase II is the actual underwriting process. It begins once a carrier is selected from the Indication Comparison Analysis.

- Seller provides access to data room and disclosure schedules. Buyer provides access to all internal, and 3rdparty diligence reports.

- An underwriting call is required between buyer deal team, buyer advisors, broker, and carrier to review diligence process.

- A draft policy is produced after the call, and policy negotiations ensue. Final form of policy is bound at singing.

- Phase II underwriting timing always matches deal timing, with typical expectations of no less than 5-7 days required to complete.

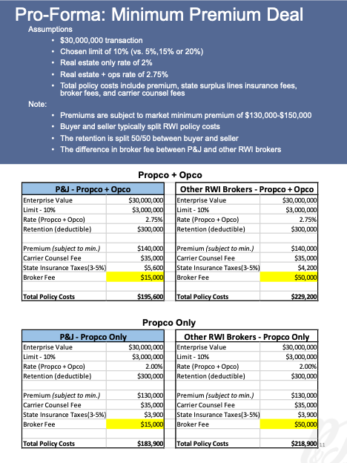

7. RWI Policy Structure & Pricing

- See Pro-forma documents for pricing and structure examples.

- Typical RWI limit is 10-20% of purchase price

- However, the amount of limit desired is determined by buyer and seller, so it can be higher or lower.

- Rates for Propco only deals are roughly 2%.

- Rates for Propco + Opco deals range from 2.5% -3.5%.

- Premium is a function of the limit X rate.

- Minimum premium ranges between $130,000-$150,000.

- A retention (deductible) of 1% of the purchase price is required. Typically, buyers and sellers are required to split the deductible 50/50, but not always as some deals are structured as a “Walk Away” deal

- A “Walk Away” deal is one where the seller’s reps do not survive closing, and the seller is not responsible for any holdback or post-closing liability whatsoever

- 90+% of RWI policies are buyer policies, with the buyer as the named insured.

- However, the seller often introduces RWI into the process first by contacting P&J in to ensure the viability of coverage. Once assurance is given, buyers can then request RWI be included on buyer’s bids with more confidence of coverage

- Buyers and sellers typically split the total costs of the policy.

8. Diligence Required

- RWI carriers do not perform their own, separate diligence. Carriers come behind the diligence that is performed by the buyer. Therefore, thorough buyer diligence is required to underwrite an RWI policy. Third party diligence, or diligence in a deliverable format is preferred/required.

- Typical diligence required is as follows:

- Financial/Quality of Earnings (QOE): A QOE is usually required. Further, if the seller does not have audited financials, a QOE is required to get coverage for financial reps.

- Tax: A tax diligence/report, ideally performed by a 3rdparty audit firm.

- Legal: A full legal report performed by M&A law firm. Expected areas of diligence including disclosure schedules, lien/bankruptcy, litigation history, compliance with applicable laws, permits and licenses, material contracts, P&C insurance history, employee benefits, and cyber/IT/IP.

- Industry Specific: Senior housing specific diligence for AL/IL/MC includes a focus on operator management, staffing levels, financials, insurance claim history, and general operator/healthcare compliance.

- Skilled Nursing: Diligence for SNF’s include all of the above, plus billing/coding audit, healthcare regulatory compliance report, and a Pepper report.

9. Why Pritchard & Jerden

- P&J was one of the first brokers anywhere in the U.S. to specialize in RWI.

- P&J is in the Top 1% of commercial insurance brokers nationwide.

- P&J’s RWI broker fees are typically 50%+ lower than the RWI broker fees for the other RWI brokers (see Pro-forma for more details on costs).

- P&J has a dedicated Senior Living & M&A Insurance Practice Group. This group handles all three phases of insurance for senior housing acquirers and operators:

- RWI for senior housing M&A deals

- M&A diligence on the target’s commercial insurance & employee benefit programs

- Commercial insurance and employee benefit placement and ongoing risk management post-close

- The overlap of expertise in all three disciplines increases efficiency and reduces costs for senior housing acquirers and operators.

- P&J had the foresight to start contacting acquirers of senior housing over a year ago. This initiative was born out of the belief that the RWI market would start moving in the direction of senior housing M&A, which is now beginning to happen on a more regular basis.

- This report itself is further evidence of our concentration and specialization in the senior housing M&A sector.

- Often-times we find risk management, legal, and business development divisions within a company are free to utilize their own relationships for RWI, as opposed to being tied to the commercial insurance relationship in place.